{kind=link}

How much money do you really need to retire comfortably? Dude I’ve been losing sleep over that exact question since roughly 2019 and I still don’t have a clean answer.

Right now I’m sitting in my kinda dark apartment in [redacted US city], it’s January 2026, there’s half a cold brew sweating on the table making rings on a printout from Vanguard that says my “projected retirement balance” is… optimistic at best. The radiator is clanking like it’s about to die and I can smell someone’s burnt popcorn from down the hall. Real glamorous retirement-planning vibes over here.

What the “Experts” Say vs. What My Gut Screams

Everyone and their financial advisor loves throwing around that 25× rule. You know—the famous Trinity Study updated a bunch of times that basically says if you want to pull 4% a year safely then save 25 times your annual spending.

So if you spend $60,000 a year after taxes in retirement → $1.5 million is the magic number.

Cool. Except my brain immediately goes “yeah but what if healthcare eats me alive” and “what if Social Security gets means-tested into oblivion by the time I’m 67” and “what if I want to actually enjoy travel before my knees give out completely”.

The 25x Rule for Retirement: Definition and Examples | Bankrate

I ran some back-of-napkin math last week while stress-eating Flamin’ Hot Cheetos and got scared. Really scared.

My Personal “Oops I Kinda Wasted My 30s” Numbers Right Now

I turned 41 last October. Current investable assets (401k + Roth + taxable brokerage): ≈ $387,000 Current annual spending (not including mortgage): ≈ $58–62k depending how much DoorDash I do when I’m depressed Mortgage left: $214k at 3.75% (thank god I locked that in 2020) Projected Social Security at 67: roughly $2,450/mo in today’s dollars according to ssa.gov quick calculator (which feels like a lie)

If I stopped contributing tomorrow and just let things compound at a very conservative 5.5% real return… I’m looking at maybe $1.1–1.2 million by 67. That’s not even close to $1.5M. And that assumes inflation behaves and the market doesn’t do 2008 again right when I retire.

So yeah. According to the classic rule I’m screwed. Or at least “comfortably middle-class retirement” screwed.

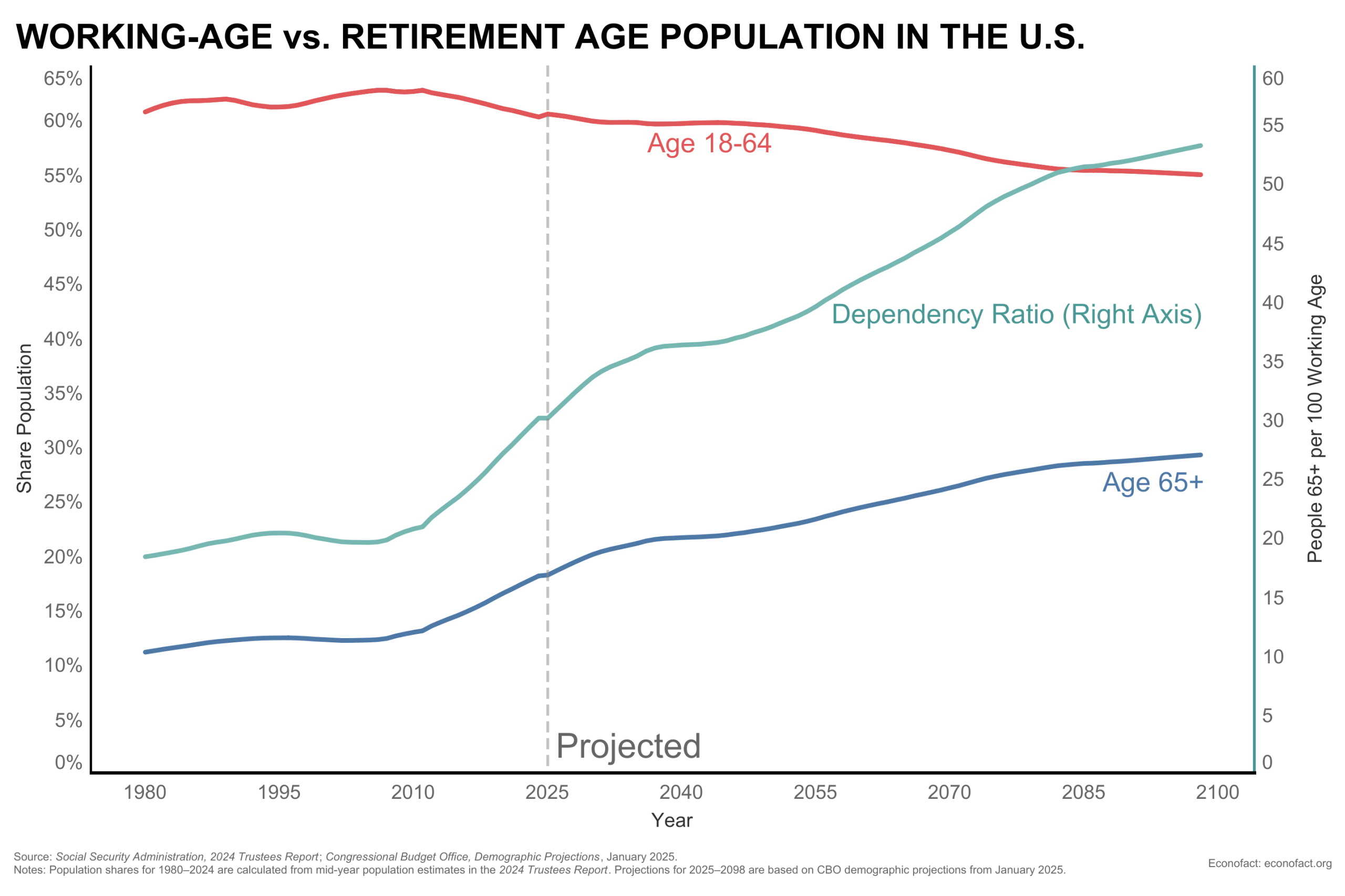

Facing the Social Security Shortfall (Updated) | Econofact

Look at this disaster. That’s real life retirement planning 2026 edition.

The Number Feels Different When You’re Actually Living It

Here’s where it gets messy and honest.

Some days I think $1.2 million would be fine if:

- I downsize the house after the kids (hopefully) move out

- I move to a lower cost-of-living state (sorry Colorado, you’re gorgeous but brutal)

- I keep doing some consulting / side hustle into my 70s because honestly I like feeling useful

- Medicare actually covers most stuff and I don’t get hit with a $300k long-term-care bill

Other days I spiral and think I need $2.5 million+ because:

- Long-term care insurance quotes are insane

- I watched both my parents burn through money on medical stuff in their last five years

- I want to be able to fly business class to Japan once before I die

- Inflation has been a sneaky bitch lately

See? Contradictions. That’s the human part.

What I’m Actually Doing (Besides Panicking)

- Maxing the 401k + catch-up contribution now that I’m over 50… wait no I’m 41. Damn. Okay maxing + mega backdoor Roth when the company allows it.

- Keeping taxable brokerage in low-cost total market funds even though the balance makes me nauseous when it drops 15%.

- Slowly paying extra on the mortgage because the psychological win feels better than optimal math sometimes.

- Trying (and mostly failing) to keep lifestyle inflation in check. That new iPhone 17 Pro Max? Didn’t need it. Bought it anyway. Classic.

- Reading Mr. Money Mustache, Early Retirement Extreme, and arguing with people in the Bogleheads forum at 2 a.m.

So… Final Answer? (There Isn’t One)

If I had to pin a number today for how much money you really need to retire comfortably—at least for someone like me who wants to stay in the US, eat out occasionally, travel once a year, and not stress about every single bill—I’m landing somewhere between $1.4 million and $2.1 million depending on how frugal / healthy / lucky I stay.

But the realest answer is: it depends so much on your personality, your health, where you live, and how much uncertainty you can stomach.